Canada’s Parliamentary Budget Officer and Stephen Harper’s nemesis and a man he wishes that he had never hired for the job, Kevin Page, has released his prognostication for Canada’s economy in his most recent PBO Economic and Fiscal Outlook (EFO). Here are some of the highlights of his independent and non-partisan analysis.

Canada’s Parliamentary Budget Officer and Stephen Harper’s nemesis and a man he wishes that he had never hired for the job, Kevin Page, has released his prognostication for Canada’s economy in his most recent PBO Economic and Fiscal Outlook (EFO). Here are some of the highlights of his independent and non-partisan analysis.The PBO opens by noting that the global economic outlook has soured since their June EFO due, in large part, to the ongoing concerns about unsustainable levels of Eurozone debt. Also playing into the equation is the slowdown in the United States economy and the downward revisions to previous quarterly growth figures which show that the 2008 Great Contraction was longer and the rebound has been weaker than originally thought. Here’s a graph showing what really happened to American economic growth once revisions were considered:

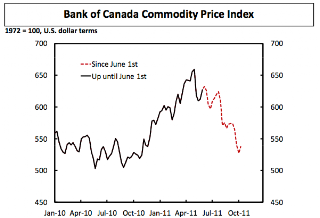

All of this has led to downward pressure on global commodity prices; this is of particular concern to Canada’s economy which hinges on the production of commodities. Here is a graph showing how commodity prices have retraced their steps to just above last year’s lows:

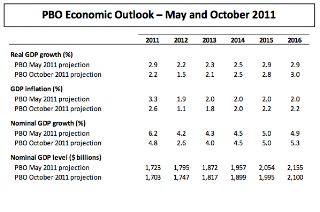

When the PBO takes all of these factors into consideration, they conclude that the level of nominal GDP will likely be $20 billion lower this year and $48 billion lower in 2012 what was expected in their May 2011 projection. Here is a chart showing the growth downgrade:

The PBO anticipates that real GDP will grow by 2.2 percent in 2011, 1.5 percent in 2012 and 2.1 percent in 2013. The growth in 2011 is 2.5 percent below the economy’s productive capacity and this gap will ultimately lead to higher unemployment. As well, the PBO is concerned that the high level of Canadian household debt will restrain growth by a significant amount and will result in less spending on residential investments. With Canada’s real estate market becoming increasingly frothy-looking, I suspect that a correction in the housing market could retard Canada’s economic growth even further than the PBO projects.

Mr. Page goes on to discuss the impact of slower growth on the Federal government’s (pardon me, the Harper government’s) fiscal situation. Let’s look at the revenue side of the ledger first. As the economy grows, budget revenues are expected to outpace growth in nominal GDP for two reasons; first, the increase in tax revenue based on growth in the economy and second, the increase in EI premiums from $1.78 per $100 of insurable earnings to $2.28 in 2016. Unfortunately, this is offset by the reduction in corporate income tax to 16.5 percent in 2011 and 15 percent at the beginning of 2012.

On the expense side of the ledger, government program expenses are projected to growth at 2.8 percent annually on average over the next 5 years with direct program expenditures expected to growth at 1.6 percent annually, well below growth levels seen in the mid-2000s but higher than what was seen in the second half of the 1990s as shown on this graph:

Unfortunately for all of us, public debt charges (interest on the debt) is projected to increase from $30.9 billion in 2010 – 2011 to $40.7 billion in 2016 – 2017 as deficit spending adds to the debt and interest rates rise to normal levels. The only thing saving our bacon right now is the prolonged period of ultra-low interest rates.

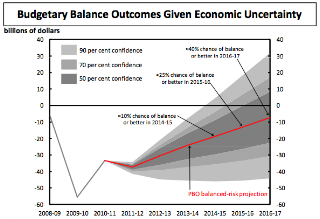

Mr. Page does note that revenues are anticipated to increase faster than total expenses including debt charges with deficits falling from $33.4 billion in 2010 – 2011 (2.1 percent of GDP) to $7.3 billion in 2016 – 2017 (0.3 percent of GDP). Here is a graph showing how he assesses the likelihood of Ottawa actually balancing its budget over the next 5 years showing that he feels that there is only a 10 percent chance of achieving balance by 2014 – 2015:

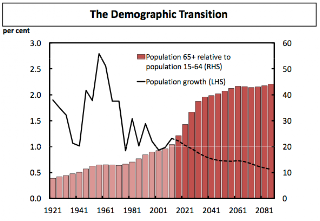

The fly in the ointment for whether or not Ottawa can achieve fiscal balance over the long term is Canada’s aging population. As the coming decades pass, increasing numbers of Canadian’s join the ranks of those who collect both their public pension and make use of their health care entitlements as shown on the red bars. The dashed and solid black line shows that there is a massive decline in the number of Canadians paying into the system at the same time as more and more Canadians are availing themselves of the nation’s pension plan and health care:

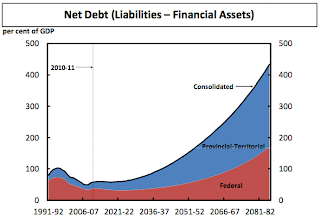

It is this demographic transition that, over the long term, will make it increasingly difficult for Canada’s federal government to achieve fiscal balance, in fact, here is a graph showing how Canada’s net combined Provincial and Federal debt will climb exponentially over the next 60 years as a percentage of GDP:

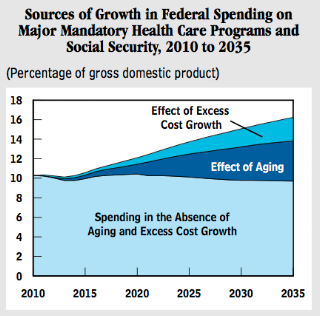

The preceding graph brings to mind this particular graph from the United States Congressional Budget Office which shows the impact of aging on growth in America’s federal spending as a percentage of GDP over just the next 25 years:

The aging issue will be faced by most of the world’s developed and developing economies, some sooner rather than later, because of a worldwide decline in birthrates over the past 4 decades. In the case of Canada, the PBO estimates that permanent policy actions that include tax increases, reduced spending or a combination of the two amounting to 2.7 percent of GDP (1.5 percent of GDP at the provincial level and 1.2 percent of GDP at the federal level) would be required to stabilize Canada’s net debt-to-GDP ratio at 58 percent of GDP. Delaying this action by 10 years will increase the amount of corrective action to 3.4 percent of GDP and waiting for 30 years will require an increase in corrective action to 5.8 percent of GDP.

It will be interesting to see whether Mr. Flaherty shows the intestinal fortitude required to keep Canada’s spending and revenue picture in balance through tax increases and staff reductions among other things. As shown here, his prognostications have been far from accurate in the past. With the Federal Reserve revising down their projections showing that growth for 2011 has dropped from 2.7 to 2.9 percent to 1.6 to 1.7 percent in just three short months, I’d suggest that the growth projections of both Mr. Page and Mr. Flaherty may both be well on the optimistic side. This will make it increasingly unlikely that the Conservatives will reach their budgetary targets.

If you want to view all Glen Asher blogs click HERE

You can publish this article on your website as long as you provide a link back to this page.

Be the first to comment